Measuring Buyback Returns

- Ryan Bunn

- Jun 15

- 4 min read

Measuring returns is an art, not a science — Proper decisions require proper measurement — Today’s tools fall short in a risky world.

MEASURING BUYBACK RETURNS

For the few businesses willing to take an active approach to share buybacks, measuring potential returns is necessary to make proper decisions. Unfortunately, measuring the return of a share repurchase can be a challenge.

Today’s tools are often insufficient to properly evaluate the risk/reward tradeoff of various investment options. Even sophisticated investors rely on heuristics or mathematical shortcuts, recognizing the fallibility of valuation tools.

This paper will review the valuation tools often used for judging buybacks and discuss their limitations.

Cash-on-Cash Returns

Investors often measure the attractiveness of buybacks by simply looking at the cash-on-cash return associated with repurchases. This measure is attractive due to its simplicity and the ability to compare returns between different capital allocation options.

But with simplicity comes abstraction. Investors often measure this return using an earnings-to-price ratio (the inverse of a P/E). Using this method, a stock trading at 20x earnings would generate a 5% return when repurchasing shares. But earnings are frequently not cash flow, so this shorthand can overestimate true cash returns.

Even when computing returns using free cash flow per share, this method ignores the future growth potential of a business, making the calculated return highly theoretical. A declining business will return less than the calculated return over time, while a growing business may deliver returns far in excess of the immediate cash-on-cash estimate.

Whatever the outcome, point-in-time cash-on-cash return calculations are likely too simplistic to reflect reality due to their failure to account for future growth.

DCFs & IRRs

DCFs and IRR calculations provide a more realistic estimate of a business’s intrinsic value and future return potential, but these valuation methods come with their own often-discussed limitations.

First, these methods require projections into the future. Each year of forecasting introduces additional uncertainty into the result. Projections more than 3-5 years into the future may result in precise estimates of returns without true predictive value. Simply deciding on how many years to forecast is a debate in and of itself.

These metrics also rely on estimates of terminal multiples or perpetual growth rates that are inherently challenging to forecast. Macroeconomic conditions and market psychology are unpredictable variables that add uncertainty to these tools.

Finally, deciding on a hurdle rate presents a further complication. Should repurchases be compared to a business’s cost of capital (which is not only difficult to calculate but also varies over time), a fixed hurdle rate, or other investment options?

The likelihood of being precisely wrong using these tools results in many management teams preferring the simplicity of cash-on-cash return calculations.

Risk-Adjusted Returns

The return measurements discussed also ignore the risk associated with buybacks. All capital allocation decisions impact a business’s capital structure, either adding to or reducing the credit risk of the business.

Risk-adjusted returns are challenging to estimate for capital allocation decisions due to the market’s poor definition of risk. If risk is defined as the volatility of a stock in relation to the broader market, then what is the risk associated with internal capex, acquisitions, or repurchasing shares? Do repurchases reduce the risk of an equity investment because they dampen volatility of the shares? Or increase the risk as leverage grows?

Just because measuring risk is difficult doesn’t make it irrelevant. Properly evaluating buybacks should incorporate an estimate of risk-adjusted returns. Today, measurement tools are insufficient to provide this estimate.

Risk In Real-Time

Highly levered businesses, due to their credit risk, often trade at low multiples. This makes the cash-on-cash return from buybacks appear to be attractive, but this return ignores risk.

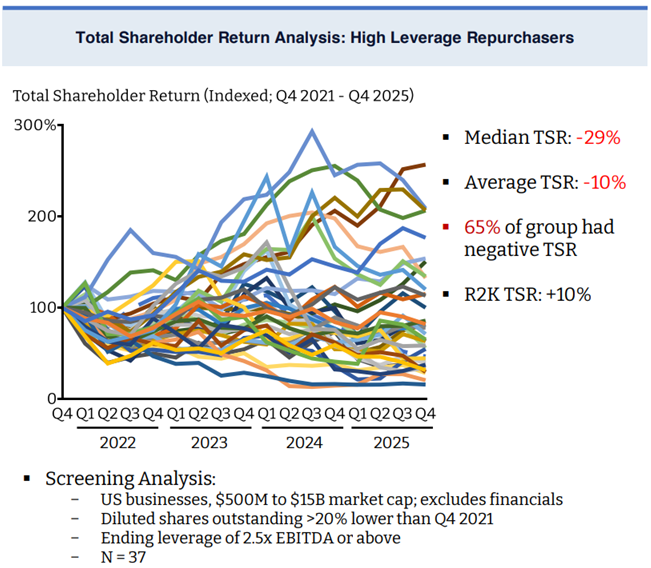

From a more straightforward view of risk, rather than share price volatility, it is clear that businesses with high levels of debt are exposed to rising interest rates. When interest rates rose between 2021 and 2025, levered businesses buying back shares underperformed, in aggregate, with a median TSR of –29% compared with a +10% increase in the Russell 2000.

Investors interested in betting on interest rates have a plethora of investment options available to directly access this risk. Investors in publicly traded equities are generally interested in the performance of the business itself, not interest rate changes.

From this perspective, the risk-adjusted returns of buybacks for levered businesses are likely to be lower than calculated cash-on-cash returns.

“You Get What You Measure”

When accounting for the uncertainty associated with future forecasts, capital structure changes, and real risk, the returns associated with buybacks become difficult, if not impossible, to measure accurately.

Repurchasing shares agnostic to price is a low-probability bet on shares outperforming. A more sophisticated but equally ineffective approach is using inaccurate or risk-ignorant return measures to time share repurchases.

Absent a reliable measure of return, repurchases default to a function of available cash flow rather than price. This results in a business having the most confidence to deploy cash precisely when valuations are highest.

This dynamic is consistent with why, in aggregate, corporate buybacks are pro-cyclical, peaking near market highs and collapsing in downturns.